Cotton is an industrial crop, grown mainly for the textile, food and cosmetics sectors. It is one of the mainstays of cropping systems in tropical and sub-tropical regions, which also include food crops. Expanding research on cotton cropping systems in the global South therefore contributes to development and to the food self-sufficiency of people in those countries.

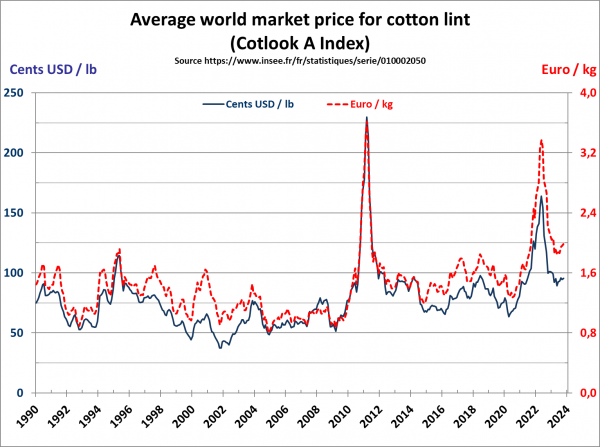

Around 26 Mt of fibre produced in 2022/2023 on 33 million hectares India and China are the leading producers and users, with the textile industry now primarily in Asia The USA is the third largest producer and leading exporter, ahead of Brasil, India and sub-Saharan Africa Fibre yields vary between 100 kg/ha/year (Africa) and 2000 (Australia) Three quarters of the area under cotton worldwide is planted with GM cotton, which is resistant to insects or herbicides 350 million jobs worldwide: cultivation, transport, ginning, packing, storage, etc. Global cotton consumption has more than doubled in 50 years At the same time, cotton's share of the global textile fibre market has fallen from 70 to less than 30% As with all commodities, cotton prices fluctuate in line with supply and demand (see chart below)

More than 100 million family farms live on the income generated by cotton in the global South Output stands at 1.1 Mt of fibre in sub-Saharan Africa, ie 4% of the global total, but represents 11% of global exports, and cottonseed is used locally to produce oil and soap .

For producers in the global South, cotton is the main source of income

In Cameroon, in 2014 (a good year), more than 200 000 farmers each, on average, cultivated 1 ha of cotton and harvested 1400 kg of cottonseed. At a guaranteed price of € 0.40/kg, that provided them with a gross income of € 568/ha. After deducting the € 215/ha of input costs (seed, fertilizers and pesticides), the annual nett profit for each farmer was € 353/ha of cotton on average. Some of that profit served to pay the casual labour required for the crop.

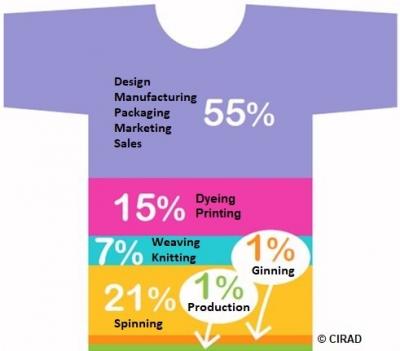

Cotton accounts for just a small share of the price of textile products

For a 150-g 100% cotton T-shirt sold for € 15 in the shops, the price paid to farmers for their cottonseed (€ 0.15) and that of the raw material (fibre, € 0.20) represent less than 3%. The latter stages of the supply chain, from design to sales, account for more than half of the price. (see schematic opposite)

The issues

Cotton is an industrial crop, grown mainly for the textile, food and cosmetics sectors.

On a global level, the issues are:

The loyalty of international competition, which is under threat from two internal influences: the weight of China in international trade and the subsidies granted to producers in developed countries.

Cotton prices on the global market. The leading producing countries are also the biggest consumers; from one year to another, they may be either nett importers or nett exporters, which makes global prices highly variable. Moreover, those prices depend on events on the futures markets and on dollar exchange rates .

Cotton's global textile fibres market share, in the face of competition from synthetic fibres. The likely eventual rise in oil prices should prompt renewed interest in cotton. To a lesser extent, the debate surrounding palm oil could benefit cottonseed oil.

In sub-Saharan Africa, production is primarily from rainfed, non-GM crops. In the most landlocked regions, cotton is often the only profitable cash and large-scale export crop. The issues are:

Rural development, particularly in landlocked countries, fostered by growing cotton in savannah zones.

The contribution of small family cotton farms to reducing food insecurity, in a context of extreme vulnerability linked in particular to climate events, degraded soil fertility and conflicts with livestock production, against a backdrop of strong population growth and increased urbanization and insecurity.

The economic and social role of the supply chain. Cotton ensures more stable monetary incomes that are less speculative than with other crops, notably food crops, and enables saving and productive investment. It also enables the development of producers' organizations and an increase in their scope.

The comparative advantages of production in relation to other cotton-growing zones, given that harvesting is done by hand and only moderate use is made of chemical inputs, which could be promoted.

Technical adaptation capacity, in the face of environmental, social and economic constraints, with a view to improving yields and productivity and safeguard product quality. Adapting to climate hazards is the dominant issue in sub-Saharan Africa, where cotton is primarily grown Under rainfed conditions, without irrigation.

Continuing research work centring on varietal improvement and cropping techniques, which is jeopardized by the limited means of national agricultural research structures and calls for international cooperation (training, scientific and technical support, regional approaches, etc.).

Product quality, which has to be tailored to target uses: quality and commercial specifications for fibre (systematic, transparent and reliable characterization, support of the regional technical centres already up and running in Mali and Tanzania); adaptation to ensure optimum dietary use of cotton products (improving cottonseed oil and protein content).

Adaptation to demands from consumers, who are increasingly concerned about social, environmental and economic conditions within production chains: recognition through labels (fair trade cotton, organic cotton, Cotton made in Africa, Better Cotton Initiative, etc.).

Revitalizing coconut, a plant with a thousand uses: knowing and making better use of its genetic diversity and ensuring sustainability, from production to processing.

.jpg)

B. Bachelier © CIRAD")